Tim turned 16 the other day. By the time Tim is 30 the world will be producing only half the oil it is producing now and when he is 40 it will be producing less than a third.

Since I found out about peak oil in 2004 I have bothered you with my dire predictions. I know we got the timing wrong, and I know we have subsequently found shale oil and the global economy has continued on a business as usual path. You think I was wrong, do you?

Well here we are at 2017 and the article I have just read several times explains why the timing was wrong. We didn’t allow for fracking and we didn’t factor in the financing of oil. But now we are stuck. You tell me where the Nafeez Ahmed article falters. He quotes from an HSBC report and that is the sixth to biggest bank in the world. The HSBC article quotes from the International Energy Agency and from a Swedish University’s energy programme. Ahmed quotes further from a recent Cornell University paper which in turn quotes a paper from the Italy’s premier agency for government research.

I know very few of you will want to read the Ahmed paper. After all it is holiday season and we all have books to read, swimming to enjoy, bike rides and tramps to accomplish and screens to attend to.

So let me summarise this paper a little, adding an odd bit for explanatory reasons:

Conventional oil peaked in 2005. Unconventional oil (shale oil, deep sea oil) peaked in March 2015. Oil is the most dense energy form human beings have ever found and nothing has yet replaced it. Consequently it is closely correlated with economic growth and population growth. The current economic system requires constant economic growth. Oil has fuelled the growth in global wealth.

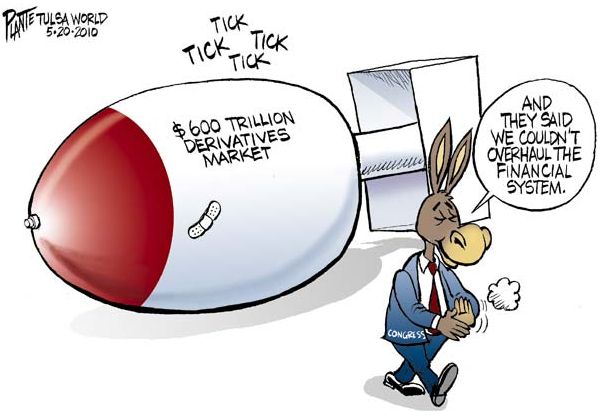

Ten years ago some of you replied, “Don’t worry, we will find something”. Oh yes we found fracking, and China went back to coal. But we also had already found debt instruments. If you don’t understand what these are you are in good company. Not even the heads of hedge funds or big banks know what strange derivatives (bets) are being invented by their traders sometimes. Ahmed says simply “the world is borrowing from the future to sustain our present consumption levels”. I know the shale oil companies were largely funded not from banks but from selling bonds. Ordinary people bought company bonds and got paid very high interest rates. The interest rates have risen so high that many shale companies are going broke paying them.

As oil exploration is yielding fewer and smaller fields and the oil is getting deeper and more expensive to extract, the oil companies abandon uneconomic fields. This happened around New Zealand and we attributed it largely to the actions of Greenpeace. But it was more than that. It costs them too much to extract it. Oil prices have recently climbed to just over $50 a barrel and companies need about $60 to break even. So they borrow. The trouble is this debt doesn’t produce real wealth.

Remember back in 2008 just before the Global Financial Crisis we had soaring oil prices? Oil went to $150 a barrel. Since nearly all goods are transported and the transport cost went up there was less money left for the rest of the economy. So we had a huge recession. So if oil prices are too high we get a recessionary effect that destabilises the global debt bubble. That debt is now higher than the pre-2008 crisis. If oil prices are too low we get too much debt which brings with it huge bank risks.

The economy can’t grow without oil. So we are stuck. The article says “the economy can quite literally never recover unless it transitions to a truly viable new energy source which can substitute for oil.”

Ahmed won’t of course have read my essay that I just submitted to the Next System Project essay competition where I propose an entirely new way of constructing a political economy so that we are not dependent on oil or on money as debt. (More of this later, I have just entered it into their international competition)

Ahmed says that because on 1 Jan 2018 there are new regulations coming into force in the finance industry, there will be a massive collapse shortly after that. He called it in 2008 and he is calling it now.

So while you are reading soothing headlines about how the economy is ‘in recovery’ or angsting over Donald Trump’s appointment of Exxon Mobil chief as Secretary of State or yet another climate change denier to a key position, think about your preparation for next year. The economy can’t recover, given its present structure and its geophysical limitations. Where will you get your food? Cash? Petrol? Will your local authority be able to maintain a good supply of drinkable water or a sewerage system if they are in increasing debt? What about power?

Now there will be those who say this is wonderful for climate change. Yes it may be the only thing that makes our planet habitable. But it is an awful way for billions of us to learn. Actually the people who will be best off will be those who are already scraping a subsistence living. But that is another matter.

If only half the today’s global oil supply is available to Tim when he is 30, what is the future for your grandchildren? Or your old age? Can you devote an hour of your precious time to getting a handle on the reality of all this? We are so privileged in New Zealand and have had it so good for so long. I have missed out on a share price boom I know. Yes I got the timing wrong. Yes I have been a doomster. But please think for yourself now. You are educated, you probably have unlimited data for your computer, use it. Plan now for a massive, tightly interconnected, global financial collapse now. You might have a year.