Land and Money, the Conjoined Twins

When there are two separate movements each claiming that they have the solutions to the world’s economic problems, we have an intellectual challenge. Rational beings might conclude each group of reformers has a key part of the truth. The two groups I refer to are the monetary reform movement and the Georgist movement.

The monetary reformers come in several varieties, but in common they believe the creation of money should be without interest and should be a public function. Privatising the right to create and control our means of exchange is the ultimate privatisation. The list of evils resulting from creating money as a monoculture with interest is long: it forces compulsory growth, concentrates wealth, causes rising debt and instability, and is generally incompatible with life on a finite planet.

So what do Georgists want? Named after Henry George, Georgists want to ensure we all have an equal right to the fruits of the earth. They seek economic justice. Since we can’t all occupy the one spot, land value taxation is the means by which those with exclusive use of the best sites or resources compensate the rest of us (who are excluded). The method of doing that is to tax land. They want to untax labour and enterprise and tax the monopoly use of land. This reduces paperwork and stimulates productivity. Business will boom. A land tax would prevent housing bubbles, arrest suburban sprawl, stop the transfer of wealth from the landless to the landowners, increase everyone’s purchasing power as incomes rise relative to prices, share the bounties of the earth and our accumulated wealth more equitably.

So what do Georgists want? Named after Henry George, Georgists want to ensure we all have an equal right to the fruits of the earth. They seek economic justice. Since we can’t all occupy the one spot, land value taxation is the means by which those with exclusive use of the best sites or resources compensate the rest of us (who are excluded). The method of doing that is to tax land. They want to untax labour and enterprise and tax the monopoly use of land. This reduces paperwork and stimulates productivity. Business will boom. A land tax would prevent housing bubbles, arrest suburban sprawl, stop the transfer of wealth from the landless to the landowners, increase everyone’s purchasing power as incomes rise relative to prices, share the bounties of the earth and our accumulated wealth more equitably.

Both arguments seem reasonable. Neither movement is popular with any current political party. Very few have ever heard of Henry George or read John Stuart Mill on land. Politicians have fought the banks since 1694 when the Bank of England was formed and banks were given the right to create the nation’s money supply and charge interest. While indigenous people have owned land communally and can understand why land should not be monetised and treated like other assets, they are wary because of historical injustices, and are very suspicious of local government when it comes to rating.

Some, like me, find themselves in both camps. And there are some in each movement who vaguely understand the other. Some monetary reformers realise that if interest rates fall, there will be another housing boom and those who own houses will reap an unearned windfall when they eventually sell. They understand there must be some built-in disincentive against land speculation but when it comes to solutions they only get as far as capital gains tax. Capital gains tax is limited because its effect is just to prevent property from coming on the market while owners wait for a law change to avoid paying it. To be effective it has to be imposed on all property at 100%. Unfortunately, current proposals by New Zealand political parties appear not to aspire to this ideal. Those in the Georgist movement have seen housing booms and watched banks charge interest on mortgages. They claim the banks are reaping what they call the ‘economic rent,’ an in-house term for the phenomenon where landowners reap the rise in land values over the years. Since these have actually been caused by the efforts of the community around them with the arrival of new businesses, government services and organisations, the windfalls should all be going to people in the form of the government, local and central.

Some, like me, find themselves in both camps. And there are some in each movement who vaguely understand the other. Some monetary reformers realise that if interest rates fall, there will be another housing boom and those who own houses will reap an unearned windfall when they eventually sell. They understand there must be some built-in disincentive against land speculation but when it comes to solutions they only get as far as capital gains tax. Capital gains tax is limited because its effect is just to prevent property from coming on the market while owners wait for a law change to avoid paying it. To be effective it has to be imposed on all property at 100%. Unfortunately, current proposals by New Zealand political parties appear not to aspire to this ideal. Those in the Georgist movement have seen housing booms and watched banks charge interest on mortgages. They claim the banks are reaping what they call the ‘economic rent,’ an in-house term for the phenomenon where landowners reap the rise in land values over the years. Since these have actually been caused by the efforts of the community around them with the arrival of new businesses, government services and organisations, the windfalls should all be going to people in the form of the government, local and central.

Within the monetary reform movement there are two main camps. There are those (Type A) who believe fervently in central government action to control the banks and create the money supply for the country. These include the American Monetary Institute, Social Credit, and the more recent Positive Money movement. The second type arises from the complementary currency movement (Type B) who argue that centrally issued national money is still a monoculture, can still cause monetary crises, can still cause inflation, is very disruptive to the economy and is politically impossible to achieve anyway because there are so many bank lobbyists for every legislator.

Within the monetary reform movement there are two main camps. There are those (Type A) who believe fervently in central government action to control the banks and create the money supply for the country. These include the American Monetary Institute, Social Credit, and the more recent Positive Money movement. The second type arises from the complementary currency movement (Type B) who argue that centrally issued national money is still a monoculture, can still cause monetary crises, can still cause inflation, is very disruptive to the economy and is politically impossible to achieve anyway because there are so many bank lobbyists for every legislator.

Let’s reflect for a moment on the historical connections between land and money and go back to the Italian goldsmiths. A decree of the year 1423 forbade all Jews of Venice to hold real estate (“pro Dei reverentia et pro utilitate et commodo loco rum”). So they became goldsmiths. People brought in their gold and the goldsmiths issued a receipt for that gold. Soon they found people using the notes for trading weren’t coming back for their gold very often. They discovered a trick: they could issue more receipts than there was gold to back it with. They lent out the notes and charged interest. And we have had that banking system ever since.

Now Jews couldn’t lend to Jews at interest, Gentiles were forbidden from lending out money at interest. Christians couldn’t lend to anyone with interest because the Christian church banned usury. But Jews could lend to Gentiles at interest. That was essentially their retaliation for not being able to own land. The Rothschild family of course comes from a line of goldsmiths. Leymann Bros, Goldman Sachs and many others join them.

In Fiji Indians can’t own land. Indians have now been in Fiji for many generations so they have become the traders. A Fijian dominated military government has been in power for many years. The moral of the story is that unless the earth is shared fairly we cannot hope to have peace or justice. Repeating an earlier sentence, since we can’t all occupy the one spot, land value taxation is the means by which those with exclusive use of the best sites or resources compensate the rest of us (who are excluded).

Now let us go back to the type of monetary reform Type B. Unfortunately so far in New Zealand complementary currencies we have known e.g. LETS (Local Exchange and Trading Systems, for trading goods without dollars) and Timebanks (for trading time without dollars) make scarcely a scratch on the national economy. Perhaps Bartercard and other trade exchanges do. If we want to reduce unemployment it is time to upscale complementary currencies by creating a currency at local authority level, together with a range of currencies operating at national level. The argument is that monetary reform of this type will create a permaculture of currencies and the consequence will be a more stable and resilient national economy. Leave the national currency alone meanwhile and introduce a range of complementary currencies until we get enough liquidity to create jobs and restore hope.

If we undertake monetary reform alone with interest rates dropping to zero or below and money being publicly issued, then the extra money in the economy goes towards land speculation and landowners grow rich at the expense of the many. Low interest rates cause excess money to go into property rather than the productive sector. To prevent this happening there needs to be a price on the holding of land. In the tsunami of dollars that hit America during 2001-2006, 40% of homes were either investment homes or second properties. Most of any country’s land is owned by corporates in central cities. But if we carry out the land tax reform alone, the money goes towards banks and the banking industry gets rich.

If we undertake monetary reform alone with interest rates dropping to zero or below and money being publicly issued, then the extra money in the economy goes towards land speculation and landowners grow rich at the expense of the many. Low interest rates cause excess money to go into property rather than the productive sector. To prevent this happening there needs to be a price on the holding of land. In the tsunami of dollars that hit America during 2001-2006, 40% of homes were either investment homes or second properties. Most of any country’s land is owned by corporates in central cities. But if we carry out the land tax reform alone, the money goes towards banks and the banking industry gets rich.

So both reforms must be undertaken together. Money and land are conjoined twins that can’t be separated. We need a solution which reforms money and puts a price on the ownership and holding of land while simultaneously taking it off income tax, sales and company tax. This is a tall order.

So both reforms must be undertaken together. Money and land are conjoined twins that can’t be separated. We need a solution which reforms money and puts a price on the ownership and holding of land while simultaneously taking it off income tax, sales and company tax. This is a tall order.

A word about the current world situation

Financial analysts like Nicole Foss and economists like Steve Keen now claim we have entered into a long depression where purchasing power will keep declining. Even as prices decline, wages decline further and faster.

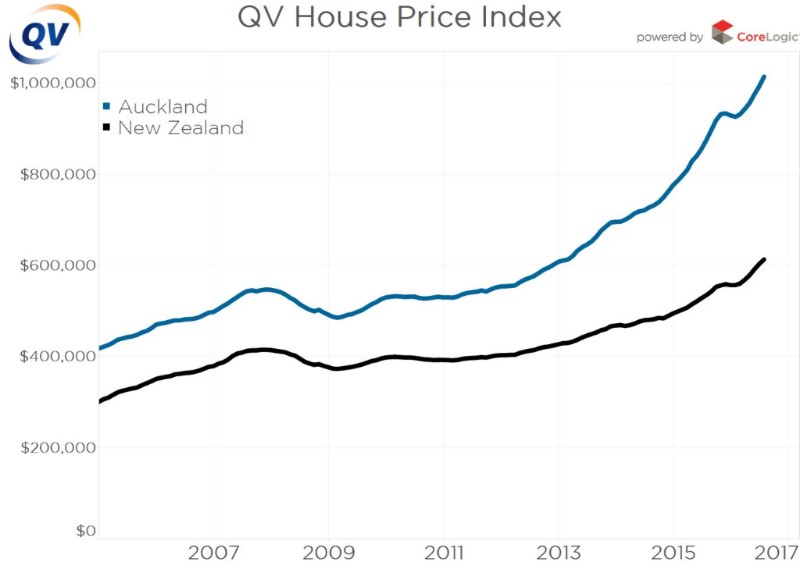

We have witnessed the largest asset bubble the world has ever seen and the bubble is bursting. House prices have fallen in Ireland and the US and this trend is coming, though unevenly, to Australia and New Zealand. Our house prices are rising in Auckland, Christchurch and Queenstown but dropping elsewhere.

In depressions thinkers  seek solutions. Henry George, a San Francisco printer, did his thinking during the 1870s depression. Silvio Gesell, a German businessman in Argentina, did his in the 1880s depression and wrote The Natural Economy. The great economist John Maynard Keynes wrote during the Great Depression of the 1930s. While a long depression will cause unending pain and disruption and may buy us time to mitigate climate change, we do need a lasting solution. This century there is a lot more at stake because global warming is proceeding at an alarming rate and our current political leaders are mindlessly locked into a monetary system requiring growth. Because of peak oil and climate change the so-called ‘developed world’ is challenged to transform in a short time period to a very low carbon economy. This time we can’t wait and must work together (fortunately with the help of the internet) for solutions.

seek solutions. Henry George, a San Francisco printer, did his thinking during the 1870s depression. Silvio Gesell, a German businessman in Argentina, did his in the 1880s depression and wrote The Natural Economy. The great economist John Maynard Keynes wrote during the Great Depression of the 1930s. While a long depression will cause unending pain and disruption and may buy us time to mitigate climate change, we do need a lasting solution. This century there is a lot more at stake because global warming is proceeding at an alarming rate and our current political leaders are mindlessly locked into a monetary system requiring growth. Because of peak oil and climate change the so-called ‘developed world’ is challenged to transform in a short time period to a very low carbon economy. This time we can’t wait and must work together (fortunately with the help of the internet) for solutions.

Three Golden Ages

So let’s have a look at history. To my knowledge there have been at least three periods when there has been both great prosperity and great egalitarianism. In their book New Money for a New Society Bernard Lietaer and Stephen Belgin describe a golden age in Dynastic Egypt for sixteen centuries up to about 30BC. Food was plentiful, there were many holidays and education was common among ordinary housekeepers and servants. They had a dual currency system with gold and silver being used for long distance trades, as well as a currency linked to the storage of food. Farmers brought ten bags of corn to the warehouse and were given a pottery receipt (an ostraka) with a date on it. When they came in a year’s time to get their corn, they were only given nine bags back. This accounted for the storage and protection against vermin. The longer the food was in storage the higher the cost. So people would not hoard the currency but spend it. Taxes were payable in ostraka and some in kind like wheat. One researcher said, “A landlord would request to have the renter of a farm pay for him the taxes in wheat owed by the landlord to that location, and that amount would be deducted from the renter’s dues.” So there was a dual currency system and a tax system based on a full land rent.

So let’s have a look at history. To my knowledge there have been at least three periods when there has been both great prosperity and great egalitarianism. In their book New Money for a New Society Bernard Lietaer and Stephen Belgin describe a golden age in Dynastic Egypt for sixteen centuries up to about 30BC. Food was plentiful, there were many holidays and education was common among ordinary housekeepers and servants. They had a dual currency system with gold and silver being used for long distance trades, as well as a currency linked to the storage of food. Farmers brought ten bags of corn to the warehouse and were given a pottery receipt (an ostraka) with a date on it. When they came in a year’s time to get their corn, they were only given nine bags back. This accounted for the storage and protection against vermin. The longer the food was in storage the higher the cost. So people would not hoard the currency but spend it. Taxes were payable in ostraka and some in kind like wheat. One researcher said, “A landlord would request to have the renter of a farm pay for him the taxes in wheat owed by the landlord to that location, and that amount would be deducted from the renter’s dues.” So there was a dual currency system and a tax system based on a full land rent.

A second economy they described which was both prosperous and stable was in the Central Middle Ages in Europe from 1040 to 1290, “the Age of Cathedrals” when there was a building phenomenon. The general populace ate well, grew tall and only worked six hours a day. Some regions had 170 holidays a year.

A second economy they described which was both prosperous and stable was in the Central Middle Ages in Europe from 1040 to 1290, “the Age of Cathedrals” when there was a building phenomenon. The general populace ate well, grew tall and only worked six hours a day. Some regions had 170 holidays a year.

There were two different types of currencies operating. One was a centralised royal coinage for long distance trading. The second consisted of an extensive network of different local currencies. There was a rather subtle hoarding charge for keeping the currency for too long without spending it. They changed the coins every time a lord died in a process called “renovatio monetae” As a rule four old coins were handed in when a lord died and exchanged for three new ones. As each coin had the same value of the coins they replaced and no one knew when the lord was going to die, it acted as a 25% tax and an incentive to spend or invest the currency quickly. The result was a great deal of building, land improvements, high quality maintenance of water wheels and windmills and enduring investments such as cathedral building. During this period the land would have been owned by a local lord and rented out to families. In other words probably the only tax they paid was on land and it was a full rental.

There were two different types of currencies operating. One was a centralised royal coinage for long distance trading. The second consisted of an extensive network of different local currencies. There was a rather subtle hoarding charge for keeping the currency for too long without spending it. They changed the coins every time a lord died in a process called “renovatio monetae” As a rule four old coins were handed in when a lord died and exchanged for three new ones. As each coin had the same value of the coins they replaced and no one knew when the lord was going to die, it acted as a 25% tax and an incentive to spend or invest the currency quickly. The result was a great deal of building, land improvements, high quality maintenance of water wheels and windmills and enduring investments such as cathedral building. During this period the land would have been owned by a local lord and rented out to families. In other words probably the only tax they paid was on land and it was a full rental.

The third period was very much shorter – in Austria during the Great Depression in Austria from 1932-1933 for fourteen months. While the national taxation system of Austria at that time needs to be researched, the local taxes would probably have only been on the value of land. Faced with 25% unemployment and declining funds, the Mayor of the small town of Wørgl thought he would put Silvio Gesell’s ideas into practice. So he put 20,000 Austrian schillings aside and spent a new currency into existence. They paid their workers in Work Certificates rather than Austrian schillings and on the back were 12 spaces. Every month the holder would need to stick a one penny Austrian stamp on the back to validate the note. This monthly stamp requirement was sufficient to act as an incentive to spend the note or invest it. Back taxes were paid and there was growing council spending on infrastructure like bridges. People came from miles around to witness what they called the “Miracle of Wörgl”. However, soon the banks put enough pressure on the Austrian government to make the whole scheme illegal, and Wörgl went back to unemployment.

The third period was very much shorter – in Austria during the Great Depression in Austria from 1932-1933 for fourteen months. While the national taxation system of Austria at that time needs to be researched, the local taxes would probably have only been on the value of land. Faced with 25% unemployment and declining funds, the Mayor of the small town of Wørgl thought he would put Silvio Gesell’s ideas into practice. So he put 20,000 Austrian schillings aside and spent a new currency into existence. They paid their workers in Work Certificates rather than Austrian schillings and on the back were 12 spaces. Every month the holder would need to stick a one penny Austrian stamp on the back to validate the note. This monthly stamp requirement was sufficient to act as an incentive to spend the note or invest it. Back taxes were paid and there was growing council spending on infrastructure like bridges. People came from miles around to witness what they called the “Miracle of Wörgl”. However, soon the banks put enough pressure on the Austrian government to make the whole scheme illegal, and Wörgl went back to unemployment.

Although caution would have to be exercised in describing these three scenarios as idyllic and there undoubtedly have been other periods in history where a measure of prosperity and happiness has been achieved, these three periods all have the following features:

- There are two currencies in operation and the local currency has a built–in penalty for hoarding money. It is a spending currency.

- A full rental is paid on land occupied and there are probably very few or no other taxes applied.

The first two eras were before the extraction of fossil fuels, while the second was in a period where there was growing oil and gas use.

Land tax, a political landmine

To invent a similar system these days provides a bigger challenge. When land taxes were an accepted feature of societies with local ‘lords of the land’ there was no income tax, company tax or sales tax. Now we are dependent on those taxes and, apart from a tiny fraction at local level, have no land tax. There may have been excise taxes imposed in Austria but it wouldn’t have significantly affected the outcome. Thus there may have been effectively only one tax operating during the Egyptian period or the Age of Cathedrals. Since all unique economies need an appropriate currency for trading, these societies each designed theirs to be a currency with an incentive to spend or invest rather than hoard.

When the idea of land tax is raised these days, there is often an immediate reaction. “I pay my mortgage on my property, I pay rates and now you want me to pay a third one? No way! The mortgage is paid to the bank, the rates to the council and now you want a tax to central government?” This is a political landmine.

These days in New Zealand we have a situation where land taxes have historically been imposed in some form at local authority level through the rating system. Local authorities used to gather in 12% of the country’s tax revenue, but now this has dropped to around 6%. At national level land taxes reached a peak of 9% of tax revenue in 1919 but these stopped in 1962. A law prohibiting land tax came into force in 1992.

The two world wars, together with a worldwide trend towards income tax, saw a great change in the tax systems. Income tax comprised 9% of tax revenue in 1909 but by 1944 it had risen to 54%. The change is probably due to the increasing power of the banks. Banks prefer income tax and hate land taxes. Income tax means banks can lend against the full value and security of land. Land tax means banks would have to lend against the security of people’s earnings power – less reliable, especially with the abolition of slavery.  2500 years ago, when borrowers defaulted, they could simply be enslaved. Now we have strong land tenure and weak “person tenure”, the land is the security to lend against. (You can get full rights over the tenure of land but you can’t get full rights over the tenure of people). Banks are higher up the “food chain” than governments. So banks get mortgage payments, governments get income tax. Our modern slavery is to the banks.

2500 years ago, when borrowers defaulted, they could simply be enslaved. Now we have strong land tenure and weak “person tenure”, the land is the security to lend against. (You can get full rights over the tenure of land but you can’t get full rights over the tenure of people). Banks are higher up the “food chain” than governments. So banks get mortgage payments, governments get income tax. Our modern slavery is to the banks.

To impose a land tax and at the same time dramatically lower income tax, company tax and sales tax, would require significant cooperation between local and national government. To seriously propose this sudden change over could be political suicide, and it would cause a huge shock for the economy. A history of the New Zealand tax system certainly doesn’t include such big jumps.

So we are faced with the challenge of not shocking the economy while moving away from taxing labour and enterprise and towards taxing what we hold or take. This includes land, including the land of the family home.

There is another reason why land tax is important. It stops the monetising of the commons (the land) and so halts the expanding of the money supply. It is this expansion of the money supply without expanding the supply of goods and services which causes inflation. Inflation robs from everyone.

We now need to reform a system where local authorities have power to tax the unimproved value of land, but increasingly opt for regressive fixed annual charges and to rate on capital value rather than unimproved value. Fixed annual charges are really regressive according to a study done by Internal Affairs in 2007. While all councils have a different mix, in the case of the Auckland supercity they are forced by statute to tax on capital value.

Various people have advocated a land tax including the commentator Bernard Hickey of interest.co.nz, while in an article by economists Andrew Coleman and Arthur Grimes in October 2011 they explore and evaluate land tax as an option. They say a central government tax could be added as an adjunct to the current system with little additional administrative cost. The authors conclude a land tax has favourable efficiency properties relative to other taxes and that a 1% land tax on all non-government land could raise approximately $4.6 billion.

The authors of The Big Kahuna, Gareth Morgan and Susan Guthrie, propose a Comprehensive Capital Tax (CCT). Capital is defined as land, buildings, structure, plant, equipment and intellectual property. There is no exemption for homeowners. Capital that consistently earns less than the required minimum rate (6% in the proposal) would face an increased tax burden. They also tax income at a flat tax on the remainder of earnings (the total earnings less required amount of earnings). The lender (the bank), having an interest in the property, also pays CCT. The authors make an excellent case for a Universal Basic Income. They argue their changes will ensure incentives to use capital productively, to use our housing stock efficiently and redistribute wealth fairly. They spread a wider net. They say they would tax anyone who owns capital in New Zealand, anyone who earns an income in New Zealand and anyone who lives here, thus encompassing any person or any corporate who owns land here or who operates a company here.

A different type of economic growth will result

For forty years since the Values Party started, green politicians have been railing against economic growth. All Budgets have been full of the phrase and many listeners have been flinching with pain for forty years. That is because what is being advocated by politicians economic growth of the type you get when you use only one currency, the national currency, a monoculture. This sort of economic growth stuffs our houses, shopping malls and landfills with electronic junk, plastic, polystyrene and nylon, clothing made using exploited labour, etc etc. When we have a land tax together with a scaled up local currency based only on what we can produce locally from the land, the type of economic growth we are going to get is quite different. It is the type we all want – growth in affordability of the basics. This includes labour to produce food from the land, revival of the local textile industry (factories in Levin lie idle as all these jobs were exported to Asia). The house maintenance industry will thrive, the biopaint industry will expand, the insulation industry using natural materials will develop and expand. With an abundant local currency designed to circulate faster than the national currency our house building will move towards using local materials. The prospects become quite exciting as we start to see a future for our semi employed friends and family and all the teenagers and young people without hope. This is a qualitatively different type of economic growth from the one we have known. The type of land tax system I am proposing is one which creates this new type of growth but not the old sick type.

And you say wouldn’t we cut down all our trees, burn all our wood for fuel or take all the fish from our waters? Wouldn’t we dam all the rivers, mine all our metal or cover our whole area with wind turbines and change our climate? The answer that in some communities this could happen if there isn’t enough awareness. Maori eliminated moa, Easter Islanders deforested their land and couldn’t build boats and Indian communities burn the dung nutrients that should be returned to the soil. Turning all your trees into charcoal (as in parts of Africa) is a disaster on many fronts.

But on the whole most communities would observe and monitor their environment and wise heads will prevent this happening. When we rely on trade for goods made with exploited labour and exploited forests we don’t notice the environmental effects because it is too far away. It is someone else’s problem. The closer a problem is to home, the more responsibility you will take.

How big should a land tax be?

It is generally understood from Georgists’ knowledge that a full rental on land is around 5% of the value of the land. In 1924 a Royal Commission named this figure as the correct percentage to impose on idle land for speculation. Only a land tax at this level can in anyway hope to replace income and company tax, let alone GST. Only a land tax at this level will discourage property speculation.

Earlier it was mentioned that we already pay mortgages and rates on land and that a third payment would be totally unacceptable. It would be politically impossible to persuade the public. The proposal that follows collapses all the payments into one. The ideas outlined in the next section address three challenges. We need to introduce a land tax without shocking the economy, to introduce a full land rental not a token one – and all the while be mindful it must be politically achievable. Land tax is not about adding another tax. It is about paying to the government rather than the bank while keeping the fruits of your own labour. The land levy proposed is payable to the local authority, it keeps banks out of the loop and uses the council income to distribute a local citizens’ dividend, thereby immediately making the system relevant to the wider public and winning their support. It designs a local currency with a built-in circulation incentive. Moreover, it provides considerable hope for a transition to a very low carbon economy in a short time period.

{kind=link}