The other morning on the radio I distinctly heard a senior politician say that the economy wasn’t going well ‘because the inflation rate was too low at below 1%’.

I thought I was hearing things. Indeed someone coming to Earth from Mars might ask a few questions. Presuming inflation is a bad thing and it is now near zero, why then is the economy not going swimmingly?

Then I remembered what I had recently learnt – that economists had designed a 1-3% inflation target as an ideal because you had to have some incentive to spend today or the economy would seize up. You didn’t want inflation too high, but a low rate of inflation is acceptable and even necessary simply because otherwise people hold on to their money and nobody spends. They realise that goods will be dearer tomorrow – if only by a little – so they decide to spend now rather than wait.

Goodness, how few people know this. And how it is becoming exposed now that the inflation is below 1% in more than one of the developed nations.

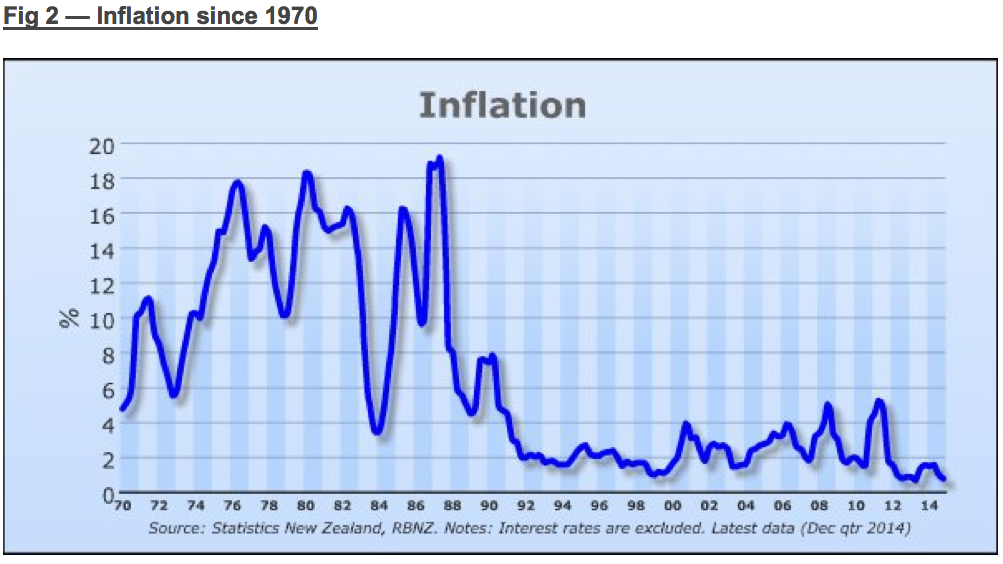

Now land was taken out of the CPI in 1999 as you can see in this graph.

Yes the graph makes good sense. With land safely out of the CPI, economists can brag that their target has been achieved for a consistently long period. And you had the huge land bubble of 2002-2008 never recorded in the CPI and then again the land bubble of 2011 onwards completely out of the graph.

So putting aside this statistical sleight of hand, we also know now that the national currency must have a circulation incentive. (That is under the current currency design of money created as interest bearing debt)

As we collectively head blindly into a period of deflation of unknown length and pain, we must pay attention to the writings of Silvio Gesell, a far thinking German businessman who also lived during a Depression in the 1880s in Argentina. His book The Natural Economic Order has been translated and put online for all to read. Of him Keynes said “The world will owe more to Gesell than it does to Marx”.

Gesell realised that a businessman with goods is at a disadvantage from those holding money. While the goods decayed, rotted and generally went out of date as they waited for someone to buy them, the money retained its value. Those in possession of money were better off than those who had goods. He famously wrote: “Only money that goes out of date like a newspaper, rots like potatoes, rusts like iron, evaporates like ether, is capable of standing the test as an instrument for the exchange of potatoes, newspapers, iron and ether.”

After decades of having loyal followers, during the 1930’s depression, Gesell’s theory was put into practice, but only briefly because the banks managed to persuade the government to stop it. It was in the small town of Wōrgl, Austria 1932 that the Mayor put aside 20,000 schillings and used them as backing for notes called Work Certificates. They paid their employees partly in Work Certificates. Each note had 12 spaces on the back and a stamp had to be stuck on every month to validate the note. To avoid paying for the stamp people spent the Work Certificates quickly. The currency was successful at reducing unemployment, so much so that people came from miles around to witness the Miracle of Wōrgl. It was in place 15 months before the government made it illegal and they went back to unemployment.